- Xi calls for a fair and equal distribution of wealth, strengthening the real economy while suppressing the virtual economy—but in doing so, he has stunted emerging industries with trillions of yuan in potential assets.

- The success of Chinese modernization hinges on striking a balance between efficiency and fairness. Most importantly, it also requires institutional reform.

- China's unwillingness to bail out the housing market may be due to Xi's insistence on shifting the focus of economic growth from real estate to technology and manufacturing.

China, the world's biggest communist power, is also the world's second-largest economy and a top manufacturing powerhouse, accounting for 18% of global GDP. If China's economy runs into trouble, it would not only affect domestic political instability and the livelihoods of its 1.4 billion people, but also global economic growth and industry supply chains, not to mention global peace and stability.

I. The Root of the Problem

1. Xi Jinping acknowledges existing problems in China's economy

On July 26, 2024, General Secretary of the Community Party of China Xi Jinping met with non-party representatives and admitted that China was facing some difficulties and problems in economic development and transformation. However, he stressed the need to have faith, insisting that the situation was entirely surmountable with some effort. He added that high-quality development would yield tangible results, leading China's economy to a brighter future.

Yet, it is worth exploring whether China's economic problems merely concern development and transformation or if they reflect medium- and long-term structural issues. In March 2024, the Wall Street Journal highlighted eight major areas of concern: slowing economic growth; a stalled real estate growth engine; lackluster consumer confidence; consumer price deflation; maxed out debt; a shrinking labor force; decline in foreign investment; and rising trade barriers.

These are the interconnected medium- and long-term structural problems confronting China today, shaped in large part by Xi's policies.

2. Xi's fixation on the real economy

The root of China's economic problems boils down to two points. First, Xi Jinping believes that production is paramount to achieving tangible results and everything else is largely inconsequential. A soaring real estate market and service-based consumption in the platform economy, such as online gaming, have done little to improve people's quality of life. This is an extremely stubborn mindset.

On October 31, 2020, Xi Jinping published an article in Qiushi, the CPC's political theory journal, emphasizing that "the real economy is the foundation of [China's] economy and manufacturing industries must not be neglected." Subsequently, sustained and massive subsidies led to overcapacity in various manufacturing sectors. Even his later concept of new productive forces merely moved overcapacity from established manufacturing products to emerging ones. The term "China Shock" refers to the impact caused by China's rapid rise in global manufacturing, the first wave of which displaced industries and jobs abroad. But with Xi's strategies extending overcapacity into emerging manufacturing sectors, China Shock 2.0 has increased cutthroat, inward-focused competition worldwide and prompted higher trade barriers against China.

The second point is that Xi has tried to gain public support—and thereby strengthen the legitimacy of his bid for another term—by cracking down on the housing market and platform-economy firms. At the end of 2016, he declared that "houses are for living, not for speculation." However, housing prices continued to reach new highs. By 2020, the government could no longer ignore the risks, introducing the three red lines policy of strict debt-ratio limits to curb escalating debt of real estate developers.

This policy was meant to limit excessive borrowing of developers and reduce financial risk, but it instead pushed many real estate firms into severe financial distress and even bankruptcy. At the same time, Xi called for fair and equal distribution of wealth, suppressing the virtual economy and youth culture in an effort to redirect resources toward the real economy and reduce reliance on foreign technology. In the end, emerging economies like e-commerce, entertainment industries, private tutoring, and gaming, together worth an estimated NT$26 trillion, were dragged down in the process.

Whether Xi Jinping's vision of Chinese modernization can succeed remains highly uncertain. China is attempting to combine macro-level control of a planned economy with micro-level efficiency of a market economy. This requires striking a balance between centralized and decentralized decision making. In other words, China must reconcile efficiency with fairness. Given China's current economic environment, domestically and abroad, this will be extremely difficult to achieve. In short, unless China undergoes institutional reform and competes fairly in the global economy, its goal of Chinese modernization will likely remain unrealized.

II. Eight Areas of Concern

1. Slow economic growth

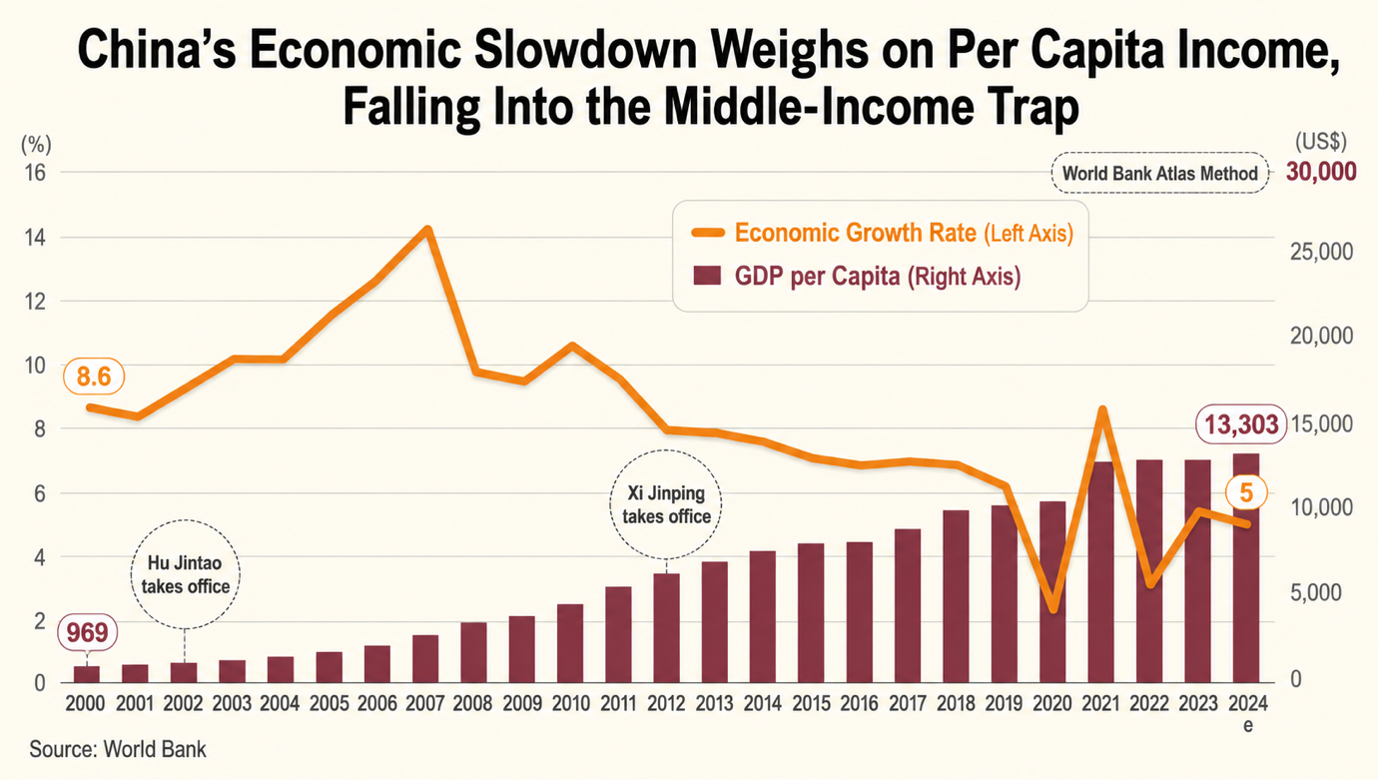

In 2012, Xi Jinping succeeded Hu Jintao as president, inheriting a vibrant economy with an annual growth rate of about 10% over the previous decade. Under Hu's ten-year leadership, China's GDP surpassed that of Germany and Japan to become the world's second-largest economy. Since Xi took office, however, the world has witnessed a clear downward trend in the Chinese economy with annual growth in his first decade falling to 6%, largely driven by weakening consumption, investment, and exports.

IHS Markit puts China's short-term economic growth (1-3 years) at 4%-5% and medium-term growth (5-10 years) falling further to 3%-4%. This is not entirely unusual as no major economy in history has been able to sustain high-speed growth indefinitely. The problem is that China's current GDP per capita is only around US$13,000. At the projected growth rate, IHS Markit estimates that GDP per capita will only hit US$20,000 by 2030, roughly equivalent to the United States in 1960. This raises concerns that China could prematurely fall into the middle-income trap.

2. Real estate growth engine stalls

Investments in real estate development account for about 20% of China's fixed-asset investment, making it a key driver of domestic demand. Observing past real estate cycles, price increases have often coincided with relaxed government regulations and loose monetary policies from the People's Bank of China. Price declines run parallel to tighter government controls and stricter policies. Therefore, government policy and monetary measures by the central bank are key to assessing the overall trajectory of Chinese housing prices.

The 2020 three red lines policy triggered widespread financial difficulties for real estate firms and left local governments relying on land-based revenue. It also sparked a wave of corporate bankruptcies, cut civil servant pay, and halted mortgage payments by homebuyers. Meanwhile, China's Real Estate Climate Index plummeted from 101.43 in 2021 to a historic low of 91.86 in March 2025. Although it slightly rose to 93.05 in August, it remains below the 100-pt threshold for a healthy market.

3. Consumer confidence takes a dive

The Consumer Confidence Index (CCI) measures the public's optimism or pessimism regarding economic outlook and personal financial situation. According to the National Bureau of Statistics of China, the index fell from a historic high of 127 in February 2021 to a record low of 85.5 in November 2022. The most recent data from August 2025 shows a modest recovery of 89.2.

About 70% of household assets in China are tied to real estate, with most households preferring to hold even more property. As a result, fluctuations in housing prices have a strong effect on wealth. When property values rise, homeowners see an increase in asset value, boosting consumer confidence and spending. Conversely, falling prices cause asset values to decline, weakening consumer confidence and consumption.

Historically, changes in housing prices tend to lead shifts in consumer confidence by six to twelve months. Given that property values in China are still in decline, consumer confidence is likely to follow, reaching a new low in the next six to twelve months. (Reference: "China's Financial Predicament: When Soaring Bank Assets Collide With a Collapsing Housing Market")

4. Consumer price deflation

In the 1990s, Japan was known as a deflationary economy and China now seems to be showing similar signs. According to the latest data from the National Bureau of Statistics, China's Consumer Price Index (CPI) fell 0.3% year-on-year in September 2025, marking two months of negative growth amid weak domestic demand and low consumer confidence. Meanwhile, the Producer Price Index (PPI) dropped 2.3% year-on-year, recording 36 months of decline since October 2022. This trend highlights how intense domestic competition puts pressure on manufacturing profits and raises concerns that consumer prices may fall even further in the future.

In the third quarter of 2018, China's weighted average interest rates were 6.19% for general loans and 5.72% for housing loans. By the second quarter of 2025, these had fallen sharply to 3.69% and 3.06%, respectively. In February 2018, required reserve ratios for large and small financial institutions were 17% and 15%, dropping significantly to 9% and 6% by September 2025. These measures, designed to make borrowing cheaper and increase the availability of credit, reflect an extremely accommodative monetary policy. Yet, considering China's economic performance, the impact of this policy has been quite limited over the past few years.

When monetary policy like lowering interest rates or increasing the money supply is unable to stimulate the economy, a liquidity trap occurs. Widespread expectations of an economic downturn lead would-be investors to hold onto liquid assets. In other words, economic actors within a country simply choose inaction. This seems to describe the current behavior of Chinese households and businesses. Though some believe China has not yet fallen into a liquidity trap, if the seventeen stimulus measures introduced in September 2024 fail to take effect in the long-term, the country may well be heading straight toward one. (Reference: "China's Faltering Consumers: Twelve Charts that Tell a Hard Truth")

5. Maxed out debt

China's Minister of Finance Lan Fo'an recently revealed that as of the end of 2024, the country's total debt had reached RMB 92.6 trillion, but remained within a reasonable range (68.7% of GDP that year). He added that risks are still manageable with ample room to implement fiscal countermeasures. But is this really the case?

Of the RMB 92.6 trillion in total debt, 34.6 trillion is from the central government, 47.5 trillion is local statutory debt, and 10.5 trillion is local implicit debt. However, the Ministry of Finance may be underestimating the scale of local governments' hidden liabilities. A July 2025 report by the Academic Center for Chinese Economic Practice and Thinking (ACCEPT) at Tsinghua University noted that as of the end of 2023, local implicit debt had already reached 14.3 trillion, with tens of trillions yet to be officially classified as central government debt. Much of this debt is held by state-owned enterprises, local government financing vehicles, or other forms, making it the biggest ticking time bomb in China's debt landscape.

Looking at China's fiscal revenues in 2024, total national revenue reached RMB 23.4 trillion, with 10.1 trillion going to the central government and 13.3 trillion to local governments. Most of the central government's revenue came from taxes collected by local governments, after which the central government reallocated these funds to poorer regions through fiscal transfers. The central government transferred 10.2 trillion back to local governments—more than its total revenue of 10.1 trillion. Essentially, even after allocating all of its revenue to the local level, the central government still had to contribute an additional 100 billion, leaving a severe shortage of funds for its own operations.

The Chinese central government needs to spend between RMB 4.5 trillion and 5 trillion each year on defense, education, foreign affairs, and other expenditures. But because all of its revenue is transferred elsewhere, these expenses are entirely financed through borrowing, posing a serious challenge to the country's medium- to long-term fiscal discipline and suggesting that China's fiscal system may be nearing a breaking point.

Data from China's Research Center for National Balance Sheet shows that when household and non-financial corporate debt is included, the debt ratio reaches 290.9% of GDP. Even more concerning, the same data shows that in 2018, the financial sector's assets were equal to 59.4% of GDP, while its liabilities amounted to 59.7%. Since then, liabilities have exceeded assets every year and net worth has remained in the negative. By 2024, the gap had only widened, with assets at 51.2% and liabilities at 70.2%.

These figures point to a sobering reality: not only is China's public finances on the verge of collapse, but its real economy and broader financial systems seem to be nearing—or already in—a state of insolvency.

6. Shrinking labor force

China's labor force began to decline in 2010. Aware of the demographic challenges created by the one-child policy, the Chinese government fully lifted restrictions to allow two children in 2016 and then three children in 2021. Yet even with looser rules, China's population growth rate continued to drop from its 1963 peak of 3.29%, ultimately running in the negative in 2021 as broader economic conditions deteriorated. According to UN projections, China will lose 42 million workers over the next decade (2024–2034). This will not only weaken productive capacity but also significantly dampen domestic demand. (Reference: "China's Demographic Reckoning: The Economic and Strategic Cost of Aging Before Prosperity")

7. Decrease in foreign investment

Not only are Chinese citizens losing hope, but foreign investors are also losing confidence in the Chinese market. According to data from the State Administration of Foreign Exchange, foreign direct investment (FDI) reached a record high of RMB 1.2 trillion in 2022, up 7% from the previous year. It fell to 1.1 trillion in 2023, a decline of 8%, and dropped sharply by 27% to just 826.2 billion in 2024. Also in 2024, net FDI outflow reached a record USD 168.4 billion, the highest level since the first-recorded statistics in 1990. Meanwhile, net inflow of FDI was only USD 4.5 billion, the lowest since 1992.

Currently, China's fixed asset investment is largely supported by state-owned enterprises, but private sector investment, including foreign capital, has fallen in the negative.

In 2024, fixed asset investment grew by 3.2%, an important contributor to the overall economic growth rate of 5%. However, while the economy expanded by 5.3% in the first half of 2025, fixed asset investment only grew by 2.8%, a far less contribution than the previous year.

Apart from real estate investment decline, corporate fixed asset investments have also shown subtle shifts. For private enterprises, cumulative growth of fixed asset investment in 2025 was 0% in January–February, 0.2% in January–April, and -1.5% in January–July. This shows that since April, fixed asset investment by private companies has not only been shrinking year-on-year but is also accelerating in its decline.

In April, China passed the Private Sector Promotion Law, but from the above data, it is unclear whether the law will be enough to stimulate the already weak private sector investment, or if businesses simply need more time to assess whether to increase investment under the current economic conditions.

Fixed asset investment by state-owned enterprises also appears to be declining month by month. If this slowdown continues, state-owned enterprise investment could see zero growth over the course of 2025.

If this decline continues, there would indeed be short-term concerns for the overall economy. However, in the medium- to long-term, reducing inefficient state-owned investment while boosting the more productive private sector investment could actually benefit China's economy.

As the world's second-largest economy with a population of 1.4 billion, China must urgently boost consumption so that it surpasses investment as a share of GDP. Only then will the Chinese economy have a chance to break free from the current middle-income growth trap of $13,000 GDP per capita.

8. Trade barriers on Chinese exports

For years, the Chinese government has unfairly subsidized its manufacturing sector, allowing many products to be sold abroad at artificially low prices and prompting resistance from other countries. According to statistics, China's annual industrial subsidies amount to nearly 5% of GDP—six times the share of South Korea, the world's second-largest subsidizer. On top of that, Chinese authorities provide low-interest loans, tax breaks, and cheap land, giving domestic manufacturers advantages other countries cannot match.

In addition, Chinese companies enjoy strong state support. Beyond low-interest loans from state-owned banks, they receive substantial tax breaks, cheap land from local governments for factory construction, discounted steel and energy, and even massive equity financing—or loan write-offs—from government-backed investment funds. These advantages have triggered growing global resistance, with trade barriers steadily rising, yet China continues to regard subsidizing its domestic companies as entirely justified.

In response to China's low-priced exports, the U.S. government began imposing new tariffs in May 2024 on key sectors including steel and aluminum, semiconductors, electric vehicles, batteries, key minerals, solar panels, and shipbuilding. The European Commission and Canada followed with similar measures in August 2024. Despite these efforts, Chinese exports have continued to expand and export prices have fallen sharply. In the first half of 2025, China's exports to the EU and ASEAN continued to grow, whereas exports to the U.S. steeply declined.

III. Expert-Recommended Solutions

1. China's economic structural problems need a one-fell-swoop radical solution

China's most pressing structural problem today is the real estate sector. The bursting of the property bubble has severely weakened consumer confidence. As a result, many observers believe that if China can decisively and comprehensively resolve its real estate problems, demand issues could largely be addressed.

Per an August 2024 Bloomberg report, the International Monetary Fund's (IMF) annual report recommended that the Chinese government adopt a "one-time solution" to complete and deliver pre-sold homes or compensate buyers. The IMF estimated that implementing this over four years would cost about 5.5% of China's GDP—equivalent to roughly $1 trillion. China rejected the proposal, citing the need to "prevent moral hazard."

However, China's largest real estate companies are still facing a dangerous situation. After Evergrande's collapse and with Country Garden teetering on the brink, Vanke Group—the country's largest developer by market value—is also facing serious financial trouble. If this downward trend continues, the Chinese government may have no choice but to adjust its approach and provide greater policy support for the housing market. The IMF notes that part of China's reluctance to intervene may stem from Xi's strong commitment to shifting the focus of economic growth from real estate to technology and manufacturing.

2. Xi Jinping must change his approach of encouraging private development while fearing it will outshine the party

In February 2024, Hideo Tsuchiya, an editorial board member of the Nikkei, wrote an article titled "China's Lost 2030: Xi's Major Economic Mistakes." The piece cites Robert Zoellick, former World Bank president, who recalled meeting Xi Jinping when he was vice president of China. "When I asked Xi about his economic priorities," Zoellick said, "he replied, 'the 86.6 million Communist Party members.'"

Evidently, Xi Jinping's primary goal at the time was strengthening the Communist Party rather than the economy. The Party takes precedence despite the economy existing to manage the country and benefit the people.

During his tenure at the World Bank, Zoellick oversaw the release of the China 2030 report, which put forward six strategic recommendations for China aimed at avoiding the middle-income trap and building a modern, harmonious, and innovative high-income society. These included: completing the transition to a market economy; accelerating open innovation; shifting toward environmentally sustainable, green growth; establishing an equitable social security system; ensuring a sustainable fiscal system; and pursuing mutually beneficial engagement with the international economy.

Had Xi Jinping properly implemented these six strategic recommendations over the past decade—especially the sixth—China's economy and the lives of its people would almost certainly not be facing the current difficulties.

According to an August 2025 report by Xinhua News Agency, Xi Jinping urged relevant departments to carefully study and incorporate public feedback on the CCP's 15th Five-Year Plan, emphasizing that citizens' suggestions have value and reflecting the planning process's principles of openness and democratic participation.

It remains unclear whether Xi Jinping has changed his earlier view that the Party takes precedence over the economy. However, his aforementioned instructions have allowed Chinese netizens to submit suggestions through a public feedback platform on topics such as education, healthcare, employment, innovation, low-carbon transition, and equitable urban and rural development. This indicates that he may wish for the next Five-Year Plan to fully reflect citizens' aspirations. The people are not asking for much—like citizens in most countries, they simply want security and a decent standard of living. The question is whether Chairman Xi will make the necessary changes to deliver that.

This article is an English translation of Chang's original Chinese-language article published on the Thinking Taiwan Chinese Edition on 11-21-2025.