- Although many countries have attempted to replicate Taiwan's contract-manufacturing model, none have surpassed Taiwan, whose model continues to evolve through technological upgrading and greater operational sophistication.

- Taiwanese companies maintain a central position in global supply chains not only through technological expertise and management efficiency, but also through an asset that cannot be easily replicated: the trust of global clients.

- As global supply chains undergo major restructuring, Taiwan's ability to strengthen its industrial foundations will depend on preserving client trust while strategically expanding investment in the United States.

Since last year, Taiwan, along with Europe, Japan, and South Korea, has actively negotiated with the United States in an effort to reduce uneven tariff burdens. Washington, however, has made large-scale investment commitments a central condition of these negotiations. The Trump administration's expectations differ from country to country, but for Taiwan, the primary focus lies in the semiconductor and electronics supply chain.

In response, the government has advanced the "Taiwan model" as the core framework for investment in the United States. Critics argue that such an approach could hollow out Taiwan and weaken its industrial foundations. Interpretations of the model vary, but sixty years of Taiwan's economic development point to a different conclusion. At a time of profound supply-chain disruption, relocating segments of the electronics and semiconductor supply chain to the United States does not signify the dismantling of Taiwan's core industries. Rather, the Taiwan model represents a pragmatic pathway for sustaining competitiveness and reinforcing Taiwan's strategic position within global supply chains.

The Taiwan Model: Sixty Years of Global Contract Manufacturing

Taiwan's economic development has been shaped by a series of major turning points. One of the most consequential occurred sixty years ago, when Taiwan successfully positioned itself within the first wave of emerging global supply chains, laying the foundation for decades of rapid growth.

At the time, American and European firms were beginning to fragment production processes and outsource manufacturing to overseas partners. Taiwan combined a low-cost but highly capable workforce with policies that encouraged investment, including export-processing zones and science parks. By seizing this opportunity, Taiwan rose alongside the expansion of global supply chains and emerged as one of the world's most important contract manufacturing hubs. As capital accumulated and technological capabilities advanced, Taiwan's manufacturing base evolved from labor-intensive consumer products—such as garments, footwear, sporting goods, radios, and televisions—toward high-tech electronics and semiconductors. Even as Taiwan moved into increasingly sophisticated production, contract manufacturing remained the foundation of its economic model for more than six decades. In broad terms, this became known as the "Taiwan model."

Other countries have long sought to replicate this approach, attempting to establish their own versions in China, Malaysia, Thailand, or Vietnam. Labor costs and land prices in many of these countries fell below Taiwan's, while export-processing zones proved relatively easy to establish. China, in particular, aspired to become the world's factory. Yet despite intensifying competition, Taiwan has never been displaced. Instead, Taiwan developed a second and more advanced version of the Taiwan model.

The Evolution of Taiwan's Manufacturing Model: Technological Upgrading and Flexible Overseas Production

This more advanced version of the Taiwan model rests on two defining characteristics. The first is continuous technological upgrading; the second is the model of taking orders domestically while producing overseas. The former can be seen in industries such as textiles, which evolved from garment manufacturing to high-performance technical fabrics, and semiconductors, which advanced from basic chip production to cutting-edge fabrication processes.

The latter reflects a deeper structural transformation. Since the 1980s, Taiwan's relationships within global supply chains have remained largely intact, but manufacturing locations have shifted—from Taiwan to China, and later from China to Southeast Asia.

This model of "taking orders in Taiwan while manufacturing overseas" reflects not only Taiwan's flexibility and resilience, but also its ability to integrate the comparative advantages of multiple economies while preserving its own core strengths. Without this second-generation Taiwan model, Taiwan's position in global supply chains over the past two decades could well have been overtaken by China, Southeast Asia, or even Mexico.

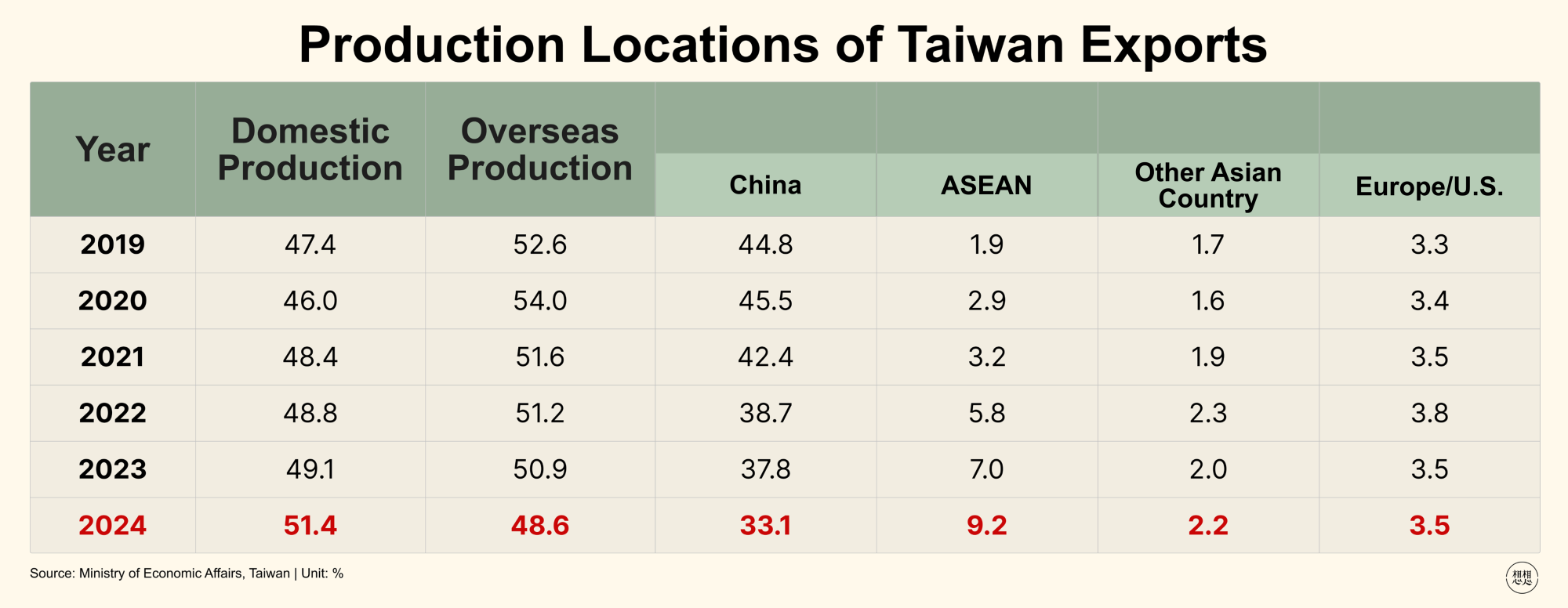

Since 2010, Taiwan's Ministry of Economic Affairs has conducted annual surveys on manufacturing patterns. Data from the past decade shows that the share of export orders produced domestically increased from 46 percent in 2014 to 51 percent in 2024. Although this suggests a degree of reshoring success, the broader structure of the model—roughly half of production at home and half overseas—has remained fundamentally unchanged.

The original version of the Taiwan model is difficult, though not impossible, to replicate. China has spent years attempting to follow Taiwan's path of technological upgrading, while Thailand, Malaysia, and India are likewise working to overcome technological barriers.

Yet regardless of which version other countries seek to emulate, one crucial ingredient remains extraordinarily difficult to reproduce. Contract manufacturing requires serving multiple competing clients simultaneously. Taiwanese firms therefore maintain their position not only through technological capability and managerial efficiency, but also through something far less tangible: trust.

This trust is built on cost competitiveness, the protection of intellectual property and trade secrets, and above all, responsiveness. Responsiveness means the ability to rapidly adjust production processes, meet shifting customer demands, and maintain close coordination with clients across changing market conditions. Over the past decade, Taiwanese firms have repeatedly demonstrated this flexibility by relocating production in line with broader supply-chain adjustments.

Surveys by the Ministry of Economic Affairs indicate that overseas relocation over the past decade has been driven less by cost reduction than by client requirements. From server manufacturing to semiconductors, Taiwan's industrial success has never depended on resisting customer demands. Instead, it has relied on flexibility, agility, and pragmatism—the willingness to adapt manufacturing locations in response to changes in the global supply chain.

A New Reality for Global Supply Chains

In all its forms, the Taiwan model remains central to Taiwan's economic growth and competitiveness. Yet it does not guarantee long-term security. Sustaining the model will require continued technological innovation, investment in human capital, and above all, the preservation of trust.

In the semiconductor sector, the United States has actively promoted the reshoring of advanced manufacturing since President Trump's first term began in 2016. Over the past decade, Washington has employed both incentives and pressure to advance this objective. TSMC is far from alone in shifting production capacity to the United States; Samsung, Apple, and NVIDIA have all moved in the same direction.

This marks another major transformation in the structure of global supply chains. From a purely economic perspective, such arrangements may not represent the most efficient allocation of resources. Yet from the standpoint of U.S.-China strategic competition and American economic security, Washington increasingly sees few alternatives. For Taiwan and the broader international community, the challenge is no longer whether supply chains will change, but how to adapt to the next several decades with flexibility and pragmatism.

Taiwan's industrial resilience is not rooted solely in the geographic concentration of high-tech clusters in Hsinchu or Kaohsiung. More fundamentally, it derives from Taiwan's indispensable role within global supply chains. By leveraging the Taiwan model—maintaining trust while expanding investment in the United States—Taiwan can preserve this strategic position while continuing to strengthen key industries. This approach may also allow Taiwan to seize the first wave of the AI revolution, much as it capitalized on the first wave of globalized manufacturing sixty years ago.

There is no doubt that large-scale investment in advanced semiconductor manufacturing in the United States will reshape existing industrial structures and generate certain negative effects. Yet smaller economies rarely have the luxury of pessimism. History also demonstrates that investments made under external pressure can still produce long-term gains.

During the 1980s, trade tensions between the United States and Japan escalated sharply over automobiles. Facing high tariffs and export quotas, Japanese automakers—including Toyota—were compelled to invest heavily in the United States. To raise the average export value of vehicles under quota restrictions, Toyota developed premium brands such as Lexus. Four decades later, the United States remains Toyota's largest overseas market, while Lexus has become one of the company's most profitable brands.

Thanks to decades of experience, Taiwan has accumulated far greater expertise than most Asian economies in managing global supply-chain networks. Moreover, because current relocation efforts are driven by economic-security considerations, many politically constructed barriers may ultimately be mitigated through negotiation, allowing governments to provide stronger support during industrial transitions.

At the same time, the long-term objective behind Washington's reshoring strategy is to secure an advantage in U.S.-China strategic competition. A complete relocation of TSMC's core operations to the United States would resemble "killing the chicken to get the eggs"—ultimately damaging both TSMC and American interests. Such an outcome therefore remains unlikely. A more plausible scenario is one in which Taiwan retains its role as the primary manufacturing hub, while selective production adjustments take place in the United States, limiting the overall impact on Taiwan. Nevertheless, Taiwan must also confront another pressing challenge: ensuring that traditional industries beyond the high-tech sector remain competitive in an era of structural transformation.

In the face of these revolutionary changes, Taiwan cannot afford either nostalgia or hesitation. The challenge ahead is to build upon the lessons of past success while continuing to evolve the Taiwan model for the twenty-first century. By doing so, Taiwan can continue to leverage its unique strengths to safeguard both its economic competitiveness and its strategic importance in the global economy.